Tourism Management: An Introduction

Additional case studies and snapshots

Read the below snapshots and case studies for examples appropriate to this chapter. Consolidate your learning by considering the reflective questions after the case studies.

The US Virgin Islands (USVI) are located in the Lesser Antilles, between the Atlantic Ocean and the Caribbean Sea. Tourism centres on the three principal islands – St Croix, St John and St Thomas – whose attractions include pristine beaches and bays, coral reefs and tropical forests. Hotel accommodation predominates, although villa rentals are also significant, and there are port facilities for cruise ships. Climate in the USVI is warm and stable with little temperature variation; average temperatures range between 25°C and 28°C, with higher rainfall from August to October, and a hurricane risk between June and November.

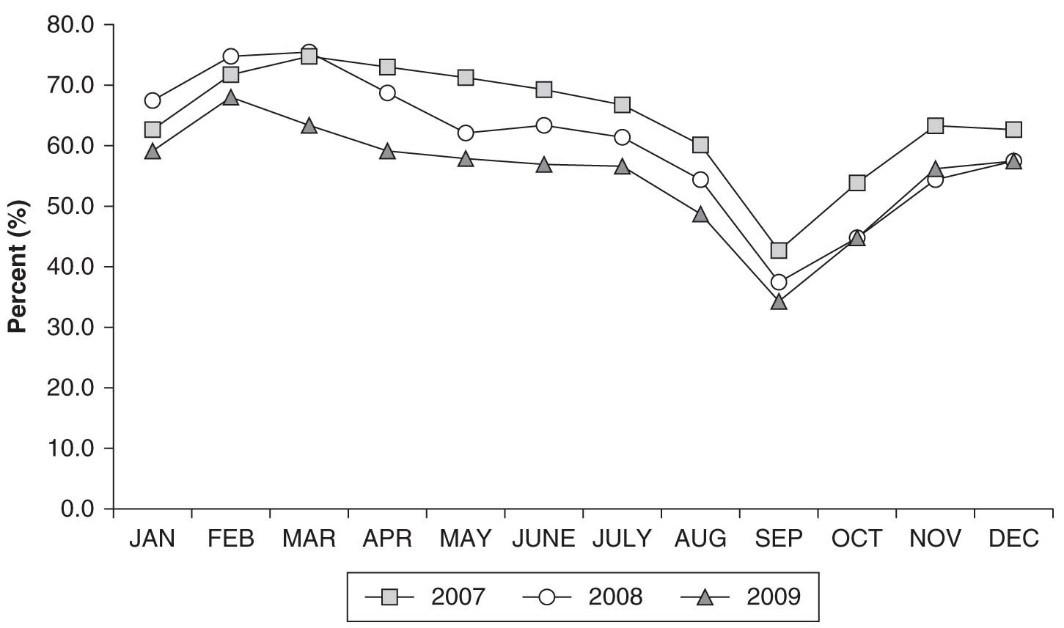

USVI occupancy rates, 2007, 2008 and 2009

Source: US Virgin Islands Bureau of Economic Research

The islands attract sunseekers, adventure tourists, MICE groups and cruise day-trippers. Annual arrivals from 2003 to 2009 fluctuated between 1.5 and 2 million cruise visitors, and 600,000–700,000 visitors by air (US Virgin Islands Bureau of Economic Research (USVIBER), 2010). The USA constitutes more than 80 per cent of the total market. Variations in demand throughout the year are reflected in the hotel occupancy rates shown in the above figure.

Although the summer is the main holiday period in the USA, demand for the USVI drops significantly. This may be explained partly by the less favourable weather in the destination, but also by improved weather elsewhere.